The impact of COVID-19 on retirement planning

With the global market falls and turbulence seen in 2020 following the outbreak of COVID-19, many pension funds have followed the stock market on its downward trajectory. In the first quarter, the pandemic inflicted the third worst week on the British stock market in history, leading 350 pension funds to fall by 25% with some even falling by as much as 50%.

Whilst many indices seem to be rallying at the time of writing (as the UK edges out of lockdown), much uncertainty still hangs over the UK economy and the equities underpinning many people’s retirement savings.

What if there is a second wave of COVID-19, for instance, which leads to another lockdown and disruption in economic activity? Until a vaccine is discovered, much remains unknown on this front.

All of this has important implications, of course, for retirement planning.

Is early retirement still a viable and desirable option at this time? Would it be wiser to postpone retirement until the wider situation has stabilised? Our financial planners here at Punter Southall Aspire turn their attention to these important questions here.

Is early retirement still a viable and desirable option at this time?

Whilst retirement lifestyles in the UK are not always mainly funded by pensions (e.g. property income may be important for some), the majority of them are. COVID-19 and the UK lockdown, is leading many people to rightly reconsider their retirement planning.

Some may still be able to retire early as planned. Others may need to think about delaying their plans or taking a lower yearly income in retirement than originally planned.

The impact of COVID-19 upon pensions has been considerable. Those nearest to retirement will likely have been most shielded from the market volatility, since much of their portfolio will probably be in “low-risk” assets such as cash and bonds.

For those in their forties and fifties who hoped to retire early within the next 5 years, however, questions will be hanging over whether or not this will still be possible. Many of these individuals are likely to have a high level of exposure to equities in their portfolios, which have taken a considerable beating in 2020.

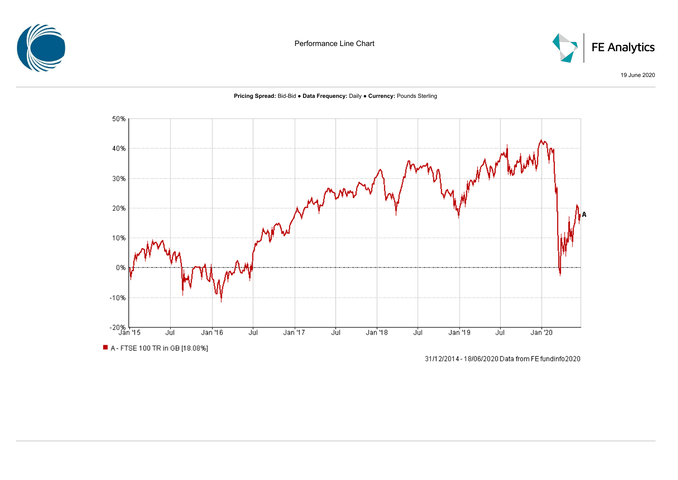

The FTSE 100, for instance, took a huge dive in March (similar to other leading indices) after the announcement of lockdown measures, leading to its worst day of performance since 1987.

As shown below, the index has been on its way up since April, yet it is still to reach the value it achieved in late December 2018. As a result of this, those with a defined contribution pension which are likely to be invested in these kinds of indices will have seen a big hit to their long term savings in 2020. Indeed, in the first quarter the average pension fund value fell by 15.2%.

Those thinking about early retirement will likely not plan on relying upon the state pension in the initial years. After all, income from your state pension only arrives in your account if you claim it once you reach your state pension age, which from October 2020 will be 66 for both men and women. Nonetheless, the state pension will almost certainly play an important role in providing an income in your later years of retirement.

The good news is that the stock market volatility of 2020 has not changed the value of anyone’s weekly state pension. The potential bad news, on the other hand, is that the state pension is a costly government expense which could be in the Treasury’s firing line to help rebalance the UK economy. Reports are starting to emerge that the “triple lock” system underpinning the value of the state pension could be scrapped in an attempt to save billions. If this transpires, it will have considerable implications for all retirement planning, not just those looking to retire early.

For those with a defined benefit pension, here your employer promises to pay you a fixed yearly income in retirement. As such, the 2020 stock market volatility is unlikely to directly affect this pension.

However, those looking to retire early need to check at which age their scheme is willing to start paying benefits.

The good news is that the stock market volatility of 2020 has not changed the value of anyone’s weekly state pension.

It might be that you need to rely on other, defined contribution pensions in the initial years of early retirement, and these have been hit by stock market volatility. Moreover, many employers themselves have had their revenues badly hit by the loss in customer purchases due to the pandemic, casting uncertainty over their futures. If the company promising your pension goes down, then this raises significant questions to raise with your financial adviser about the implications for your pension planning.

Many people in the media are arguing that early retirement is no longer a plausible option in 2020. As financial advisers we need to stress that each person’s case needs to be judged upon its own merits, and it is unwise to make blanket statements about early retirement. For certain, many people may need to delay their early retirement plans until their investments start to recover, but it’s also true that many people who were approaching their planned retirement date had already moved to a much more “defensive” portfolio before the outbreak and lockdown started. As such, these individuals might still have substantial savings which could still be used to implement a viable early retirement plan.

The crucial point, however, is that those hoping to retire in the coming years review their plan with a professional financial adviser, to ensure that everything is still on track and to check whether any sensible adjustments are required.

Each person's case is unique - those hoping to retire in the coming years should review their plan with a professional financial adviser.